May 5, 2026

A lot of Big Law attorneys I talk to are sitting on a mountain of cash that they don't know what to do with. They've worked incredibly hard to accumulate it, and now they're completely paralyzed at the idea of deploying it toward their goals. The frustrating reality is that while they're stuck in neutral, their money isn't just sitting there doing nothing. In many cases, it's actively working against them.

Think about it this way: if your cash is sitting in a checking account earning 0.01%, but you could be in a high-yield savings account earning 3%, you're quietly losing 3% per year in opportunity cost. And if that money is in a high-yield savings account when it should be invested in the market for a long-term goal, you're potentially leaving 4% to 5% or more in annual returns on the table. Over a Big Law career, that kind of inefficiency can cost you six or, in extreme cases, seven figures.

If this sounds familiar, here's how I suggest you proceed, so your money actually works for you, not against you.

Step 1: Map Out Your Goals on a Timeline

Before you move a single dollar, you need to get crystal clear on what you're actually trying to accomplish. Are you trying to pay off your student loans before leaving Big Law? Reach financial independence by 50? Buy a bigger house in the next couple of years? The answers to those questions determine everything else.

My recommendation is to map out your goals on a timeline like the one below. Write them down with target dates attached to each one, so nothing sneaks up on you at the last minute. For example, if your plan is to eventually leave Big Law and you know that paying off your student loans is what unlocks that freedom, you don't want to be burned out and ready to quit, only to realize you're still six figures in debt. The timeline forces you to be proactive rather than reactive.

This kind of goal clarity is also what separates attorneys who feel in control of their finances from those who feel like their income is just disappearing into a black hole each year.

Step 2: Create Your Money Buckets

Once your goals are mapped out, the next step is to create a dedicated account, or "bucket", for each one. This keeps your money organized, prevents you from accidentally spending funds you meant to save, and allows each pot of money to have its own investment strategy.

The key question when opening each account is: how soon do I need this money? Here's a simple rule of thumb I use with clients:

If your goal is less than 2 years away, keep that money in cash, specifically in a high-yield savings or money market account. This applies to things like a home purchase, major renovations, a planned career transition, or any other near-term goal. The runway simply isn't long enough to take on market risk. If the market drops right when you need the money, you're in a worse position than when you started.

If your goal is two or more years away, the conversation changes. Historically, the market has always recovered after a downturn, and that recovery takes about 18 months on average*. If you have a timeline of more than two years, a market downturn during your accumulation period would likely recover before you need to use the funds. This makes you better off than holding cash.

A few goals also come with specific account types worth noting:

- If paying for college is on your horizon, a 529 plan is built for that purpose.

- If you're carrying high-interest credit card debt, that's its own "bucket." It needs to be filled aggressively before you start directing cash anywhere else.

Step 3: Fill Your Money Buckets

With your buckets open and your goals prioritized, now you need to decide how much cash flows into each one. Go back to your timeline and ask yourself: which goal has the highest stakes if I fall behind? That one gets funded first.

For shorter-term goals (e.g., leaving Big Law, buying a home, etc.), it may mean keeping a larger portion of your cash in high-yield savings and making aggressive loan payments. For longer-term goals like early financial independence or college funding, that money needs to be invested in the market to grow at a rate that actually gets you there.

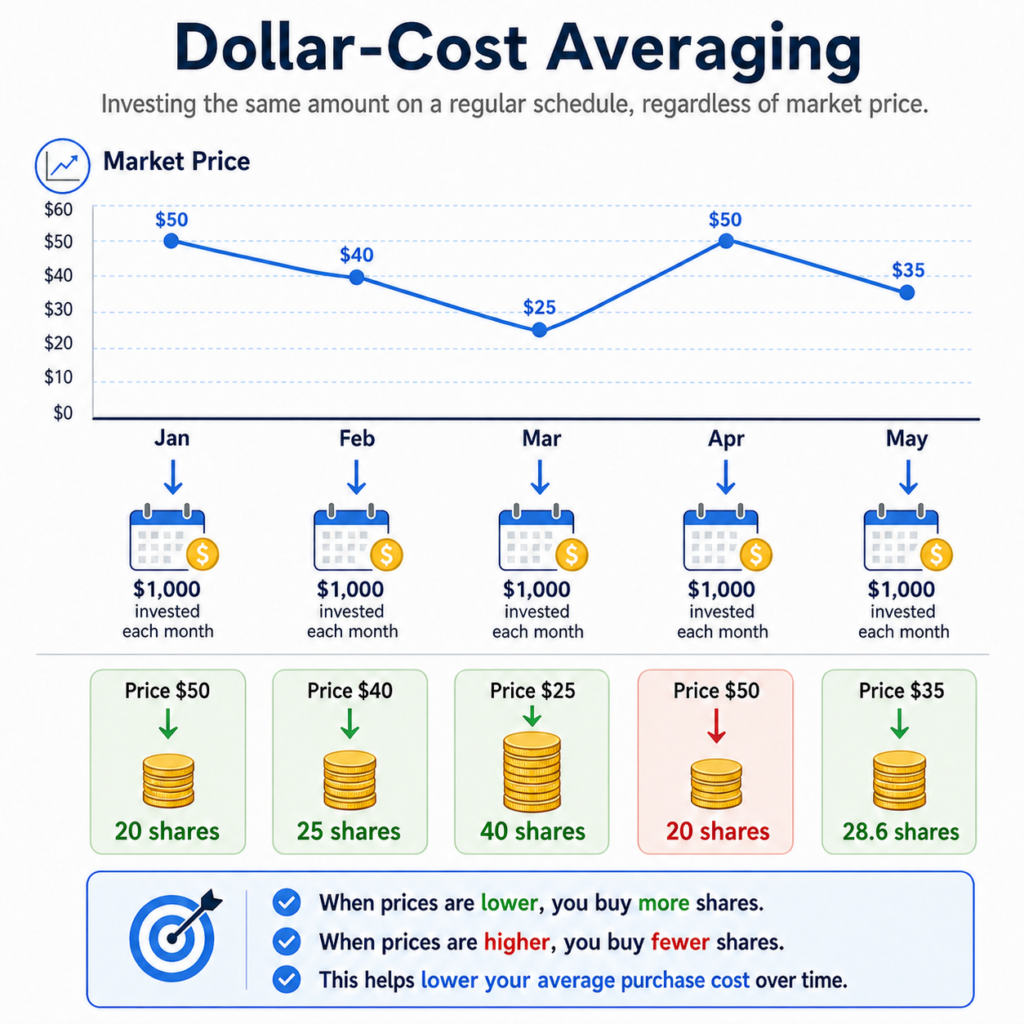

Deploying a Large Cash Position using Dollar Cost Averaging

If you have a significant chunk of cash sitting on the sidelines that needs to be invested, the worst thing you can do is dump it all into the market at once — especially if you're new to investing or you're staring at a volatile market. Instead, I recommend a strategy called Dollar Cost Averaging (DCA).

Rather than investing everything in one shot, you break it up into equal installments over a set period (3, 6, or 12 months are all common windows). Here's why this works so well. As shown in the illustration below, when markets are up, your fixed dollar amount buys fewer shares. But when markets are down, that same dollar amount buys more shares at a discount. Over time, this lowers your average cost per share, which means more money in your pocket when the value eventually climbs.

The second benefit is psychological. By spreading your investments out, you remove the risk of putting everything in on a Friday and watching the market drop 10% by Monday. It takes a big, scary decision and turns it into a simple, automated process.

And that word — automated — is the key to making DCA actually work. If you're manually deciding when to invest each month, you're going to see a scary headline, hesitate, and end up right back where you started: cash sitting on the sideline, doing nothing. Whether you work with a financial planner or do it yourself through a brokerage's automatic investment tools, the goal is to take the emotion out of the equation entirely.

One last note: while your cash is waiting to be deployed through DCA, make sure it's at least sitting in a high-yield savings account earning some interest in the meantime. There's no reason to let it idle in a bank account earning next to nothing.

The Bottom Line

If you're a Big Law attorney sitting on a pile of cash and feeling overwhelmed, the answer is not to rush into the market blindly — but it's also not to do nothing out of fear of making the wrong move. The goal is to stop thinking of your savings as one giant, intimidating pile of money and start thinking of it as specific buckets tied to specific goals.

Some of that cash might need to stay safe in a high-yield savings account because you need it within the next year or two. Some of it might need to go toward your student loans or a 529 plan. And some of it might need to be invested for the long haul. Getting clear on which dollar belongs in which bucket is what moves you from paralysis to having a real plan.

Ready to Take the Next Step?

This is the type of work I do with Big Law clients every day — mapping out goals, opening the right accounts, and prioritizing where each dollar goes. If you're not sure how to deploy your cash or want a second set of eyes on your financial picture, I'd love to help.

📅 Schedule your free introductory call

💼 Learn more about our services & pricing

*Assumes SP 500 Index Total Returns (TR) from peak to recovery for bear markets (20%+ decline) over the past 50 years (1976-2026).

SharpEdge Financial LLC is a registered investment adviser registered with the State of Texas. Registration does not imply a certain level of skill or training. The views and opinions expressed are as of the date of publication and are subject to change. The content of this publication is for informational or educational purposes only. This content is not intended as individualized investment advice, or as tax, accounting, or legal advice. Although we gather information from sources that we deem to be reliable, we cannot guarantee the accuracy, timeliness, or completeness of any information prepared by any unaffiliated third-party. When specific investments or types of investments are mentioned, such mention is not intended to be a recommendation or endorsement to buy or sell the specific investment. The author of this publication may hold positions in investments or types of investments mentioned. This information should not be relied upon as the sole factor in an investment-making decision. Readers are encouraged to consult with professional financial, accounting, tax, or legal advisers to address their specific needs and circumstances.