By Joel Chouinard, CFP®

March 26, 2026

If you're a high-earning attorney who donates to charity, a recent change in tax law might be costing you thousands each year. The "One Big Beautiful Bill Act" (OBBBA) has altered the rules for charitable deductions, and many high earners are losing out without realizing it. The good news is that a simple adjustment to the timing of your gifts can help you recover those lost deductions and make your charitable giving more tax-efficient. Want to ensure your giving does the most good for both your causes and your finances? Read on.

How a Recent Tax Law Impacts High-Earning Attorneys

Under OBBBA, the IRS created a "floor" for deducting cash charitable contributions, set at 0.5% of your Adjusted Gross Income (AGI).

What does this mean for you? It means the first portion of money you donate each year may not be deductible on your tax return.

The Hidden 0.5% Floor on Deductions

Let's look at a practical example. Suppose your AGI is $500,000 per year, and you donate $12,000 annually to your favorite nonprofits.

Because of the 0.5% floor, the first $2,500 you give is not deductible ($500,000*0.5%). The IRS only allows you to deduct the remaining $9,500. If you're in a 35% tax bracket, losing that $2,500 deduction results in a $875 tax hit every year.

A $875 tax hit might not seem like much in a single year, but if you compound that over a 30-year career, it adds up. You could end up losing tens of thousands of dollars in tax benefits.

This rule tends to affect high-income earners who donate regularly but are not mega-donors using complex trust strategies. If you simply write checks or set up recurring donations, you may be vulnerable to this tax trap.

Keep in mind, this floor only applies if you itemize your deductions on Schedule A. If you take the standard deduction, the rules are different. The law allows those taking the standard deduction to deduct up to $1,000 (if single) or $2,000 (if married) in addition to their standard deduction.

What Is Donation Bunching?

If you itemize deductions and want to get around this tax floor, you need a proactive plan. A highly effective strategy for this is donation bunching.

Donation bunching means grouping multiple years of charitable contributions into a single tax year. By doing this, you can clear the IRS floor once, rather than letting it reduce your deductions year after year.

A Real-World Example

Let's go back to the person with a $500,000 AGI. Their deduction floor is $2,500. Suppose they typically donate $12,000 each year.

If they stick to their normal routine, they donate $12,000 but only get to deduct $9,500 ($12,000 minus the $2,500 floor). Next year, they do it again, losing that $2,500 deduction every single year.

Now, let's look at the bunching strategy. Instead of donating $12,000 every year, they combine two years' worth of donations into one. They donate $24,000 in year one.

The $2,500 floor still applies to that year, but now they can deduct $21,500 on their tax return. In the second year, they donate nothing, so the floor isn't a factor.

By grouping donations, the floor only affects them every other year. The net result is that they recover about $2,500 in deductions every two years. Over multiple decades of charitable giving, this simple change can save you thousands of dollars taxes.

This is especially critical if your income grows, as it often does for Big Law attorneys. As your income rises, your AGI floor increases, making the bunching strategy even more valuable.

Overcoming Cash Flow and Budget Challenges With Charitable Donations

While donation bunching makes sense on paper, it does present two practical challenges.

First, you might not have double your annual charitable budget in cash, ready to donate at once. Second, charities often rely on a steady stream of income. If they expect your contributions, making them wait a year could affect their budget.

Fortunately, there are ways to execute this strategy while managing your cash flow and supporting your charities.

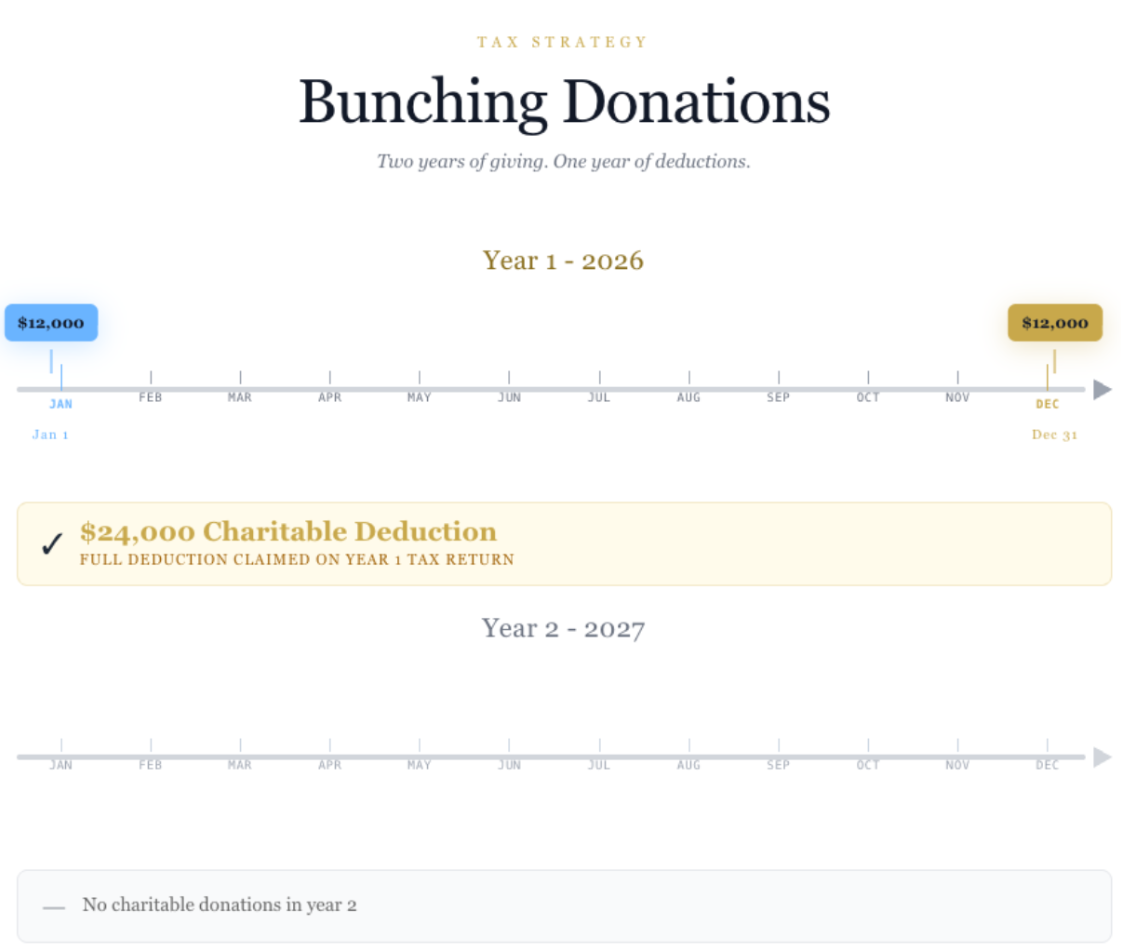

Strategy 1: The Double-Year Dip

If you normally give a lump sum each year, you can bunch your donations by carefully timing them. The graphic below illustrates this.

Make your first charitable contribution in early January. Using the $12,000 example, you could write a $12,000 check on January 5th.

Then, wait until the very end of that same year to make your second donation. You could write another $12,000 check on December 28th.

The following year, you give nothing.

From a cash flow standpoint, you still had nearly 12 months between the two donations. From the charity's perspective, they still receive money roughly every 12 months.

However, from the IRS's perspective, both donations happened in the same calendar year. You've successfully bunched $24,000 into one tax year, minimizing the impact of the AGI floor.

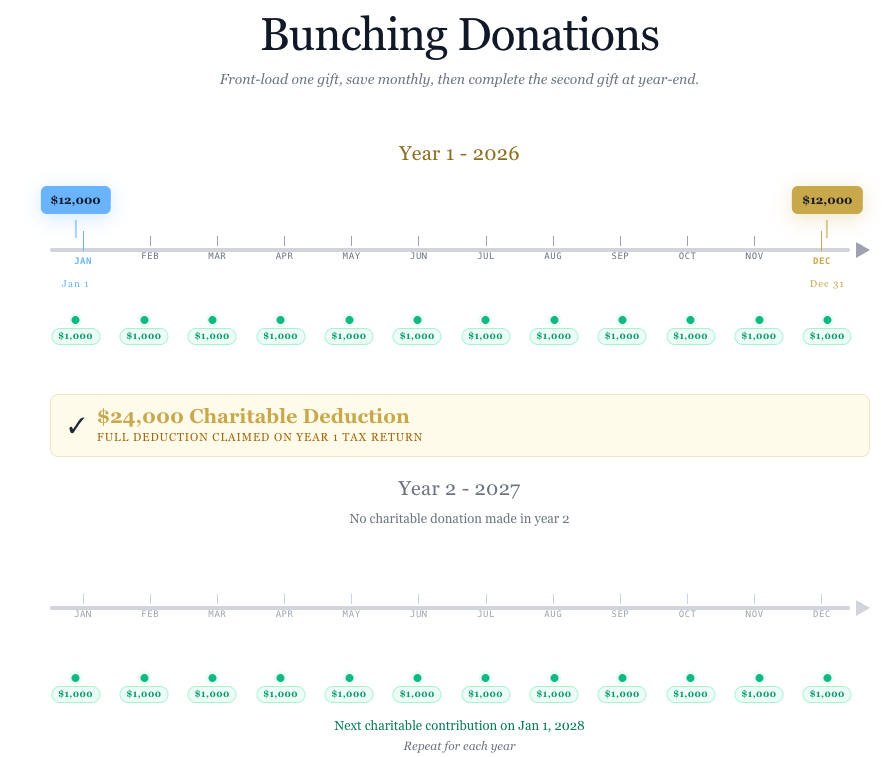

Strategy 2: The High-Yield Savings Method

If you normally give on a monthly basis, the bunching strategy requires a bit more planning, as illustrated in the graphic below.

In year one, you'll need to pre-fund the strategy. Make your full yearly contribution at the beginning of the year, say, paying $12,000 in January.

At the same time, open a high-yield savings account. Set up an automatic transfer to save $1,000 into that account every month. This replaces the monthly cash outflow you used to send to the charity.

By the end of December of that same year, you'll have $12,000 saved, plus interest. You then withdraw those funds and make your second donation right before the year ends. You've bunched two years into one.

In year two, you continue funding your savings account with $1,000 a month but make no charitable donations.

At the start of year three, you take the $12,000 from your savings and donate it in early January. Then, you resume saving $1,000 a month until December, when you make your next donation.

This method requires one upfront lump sum to start (perhaps funded from a year-end bonus), but after that, your monthly cash flow feels the same as before. The difference is that you may now receive a significant tax benefit.

Why Timing Is Everything

The recent tax law changes didn’t alter how much you care about the causes you support, but it did change how you might be rewarded for it.

For high-earning attorneys, doing nothing could mean passively losing thousands in valid tax deductions. Implementing a donation bunching strategy doesn't mean you have to give more; it simply means being strategic about the timing.

By structuring your donations this way, you can optimize your tax returns, protect your hard-earned money, and continue supporting the organizations that matter to you.

Need Help Making a Plan?

It’s important to remember that charitable giving is only one piece of your overall financial planning puzzle. Integrating your philanthropy goals with tax, cash flow, and estate planning needs careful coordination.

If you’re looking to build a comprehensive financial strategy or navigate the latest tax law changes, these decisions benefit from professional guidance.

Ready to take the next step?

📅 Schedule your free introductory call

💼 Learn more about our services & pricing

SharpEdge Financial LLC is a registered investment adviser registered with the State of Texas. Registration does not imply a certain level of skill or training. The views and opinions expressed are as of the date of publication and are subject to change. The content of this publication is for informational or educational purposes only. This content is not intended as individualized investment advice, or as tax, accounting, or legal advice. Although we gather information from sources that we deem to be reliable, we cannot guarantee the accuracy, timeliness, or completeness of any information prepared by any unaffiliated third-party. When specific investments or types of investments are mentioned, such mention is not intended to be a recommendation or endorsement to buy or sell the specific investment. The author of this publication may hold positions in investments or types of investments mentioned. This information should not be relied upon as the sole factor in an investment-making decision. Readers are encouraged to consult with professional financial, accounting, tax, or legal advisers to address their specific needs and circumstances.