May 5, 2026

Making partner is one of the biggest financial milestones of your legal career, but it also comes with a problem most partners don't see until it's too late. Your income has likely outpaced your disability insurance coverage, leaving a gap between what you earn and what you'd actually receive if you couldn't work.

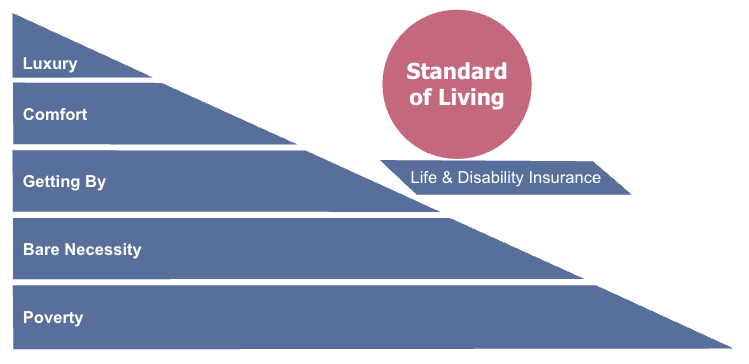

Here's the right way to think about disability insurance: it's not meant to keep you living large — it's what keeps a bad situation from becoming a catastrophic one. It's meant to stop your family's standard of living from sliding down the wrong end of this pyramid.

Here's how to figure out exactly how much coverage you need to hold that line.

Step 1: Determine Your Essential Monthly Expenses

Before you can size your disability coverage, you need a clear-eyed picture of your monthly spending, but not all of it. Here's the reality check: if you became disabled tomorrow, you probably wouldn't be booking business-class flights or funding your lifestyle at full throttle. You'd hunker down until the storm passes. You'd cut back on the extras. What you can't cut back on are your essential expenses like mortgage, utilities, groceries, insurance premiums, debt payments, etc.

That's the number you're trying to protect.

For a step-by-step process on how to calculate your essential monthly expenses, refer to Step 2 of this article.

Step 2: Determine Your Net After-Tax Existing Coverage

Most Big Law firms offer group disability plans, and most of the time, the firm foots the bill. That's great until you realize it means your benefit is taxable income when you receive it. You can't just look at your monthly benefit number and call it a day.

Here's how to think about it: if your group plan pays $25,000/month, that's not $25,000 in your pocket. You need to adjust for taxes. And no, you shouldn't assume you'll be taxed at your current rate. A disability would drop your income significantly, which changes your tax bracket.

As a rule of thumb:

- 30% tax rate if you live in a state with no income tax

- 40% tax rate if you live in a high-tax state like New York or California

- If your spouse earns income, factor that in too, as it affects your combined bracket

Using the example above: a $25,000/month benefit at a 40% effective tax rate leaves you with $15,000/month after tax ($25,000 × 0.60).

One exception: if you pay your own group plan premiums, your benefit is tax-free, so no adjustment is needed.

Step 3: Calculate Your Disability Income Gap

This is the easy part. Once you've got your essential expenses and your after-tax existing coverage, the math is straightforward:

Individual Coverage Need = Essential Monthly Expenses − Net After-Tax Existing Coverage

Using the numbers from our example: $20,000 in essential monthly expenses minus $15,000 in after-tax group coverage leaves a $5,000/month gap. That's the number you need to close with an individual policy.

Step 4: Cover The Gap With An Individual Policy

This is where most partners get tripped up, not because they don't buy coverage, but because they buy the wrong coverage. A generic individual disability policy won't cut it for a law firm partner. You need a policy built for your situation. Here are the features that matter most:

- True Own-Occupation: Pays your full benefit if you can no longer perform your specific legal specialty, even if you're technically capable of working in another field. This is non-negotiable for attorneys.

- Residual / Partial Disability Rider: If a medical condition forces you to scale back your hours but doesn't put you completely out of commission, this rider pays a proportionate benefit. Critical for partners billing at high hourly rates.

- Future Increase Option (FIO): As your partnership earnings grow, this rider lets you increase your monthly benefit without going through another medical exam. Lock it in early.

- Non-Cancelable and Guaranteed Renewable: Your insurer can never raise your premiums or change your policy terms. What you sign is what you keep, all the way to retirement.

- Mental & Nervous / Substance Abuse Extension to Age 65: Standard policies typically cut off mental health and burnout claims after 24 months. This rider extends that coverage to age 65, which is especially important in a profession where stress-related disability is a real risk.

Bottom Line

Disability insurance is a math problem, not a guessing game. Most Big Law partners have some coverage through their firm, but firm coverage alone rarely closes the gap, especially once you account for taxes and the reality of what it actually costs to run your life. Work through the four steps above and you'll know exactly where you stand. The goal isn't to over-insure. It's to make sure a disability doesn't derail everything you've spent your career building.

Need Help Making A Plan?

If you've run the numbers and want a second set of eyes, or you'd rather skip the spreadsheet entirely, I can help. I work specifically with Big Law partners and associates to address these types of decisions.

📅 Schedule your free introductory call

💼 Learn more about our services & pricing

About SharpEdge Financial

SharpEdge Financial is a fee-only financial planning firm serving Millennial and Gen Z attorneys. Whether you’re just starting out in Big Law or approaching a career transition, we’re here to guide you through the complex decisions that come with high-income professional life.

What does fee-only mean? Our clients pay us to give them holistic, unbiased advice. That’s it. We do not sell commission-based products, so we have the freedom to develop your financial plan and investment strategy free of outside influence.

Are you a fiduciary? The fiduciary standard is the highest standard of care. As a fiduciary to our clients, we always make recommendations that are in your best interest, not ours.

Why are you independent? As an independent Registered Investment Adviser, we have the flexibility to serve our clients in the way that best meets your needs. No outside influence from a large corporation.

For other FAQs, click here.

SharpEdge Financial LLC is a registered investment adviser registered with the State of Texas. Registration does not imply a certain level of skill or training. The views and opinions expressed are as of the date of publication and are subject to change. The content of this publication is for informational or educational purposes only. This content is not intended as individualized investment advice, or as tax, accounting, or legal advice. Although we gather information from sources that we deem to be reliable, we cannot guarantee the accuracy, timeliness, or completeness of any information prepared by any unaffiliated third-party. When specific investments or types of investments are mentioned, such mention is not intended to be a recommendation or endorsement to buy or sell the specific investment. The author of this publication may hold positions in investments or types of investments mentioned. This information should not be relied upon as the sole factor in an investment-making decision. Readers are encouraged to consult with professional financial, accounting, tax, or legal advisers to address their specific needs and circumstances.