By Joel Chouinard, CFP®

March 12, 2026

If you have six-figure student loans, there is a good chance those loans are quietly deciding how long you need to stay in your current job. Attorneys frequently want to go in-house, take a break, or start a family, but feel stuck because their debt balance is calling the shots.

The good news is you can pay off your loans faster without giving up flexibility or paying more interest than you need to. As you approach partnership or consider your exit options, having a clear strategy for your debt is critical.

The first step is to determine your ideal payoff date. You want a specific date in the future so you can work backward to build the best plan. Whether you want to leave Big Law by a specific date or start a family, answering this question gives you your timeline.

Once you have your target date, you generally have two options. You can either refinance with a private lender to match your loan term with your repayment date, or you can stay with your current loans and make aggressive principal payments.

Option 1: Refinance With a Private Lender

Refinancing your federal student loans with a private lender has huge implications. The most significant change is that you lose the government protections that come with federal student loans.

For example, if you lose your job, you lose the ability to go back on an income-driven repayment plan or take advantage of forbearance options. If you experience hardship, you still have to pay your loans. You also lose access to forgiveness programs, whether that is Public Service Loan Forgiveness or a death discharge.

Another easily overlooked factor is the amortization schedule. When you take out a new private loan, you reset your amortization schedule. You may secure a lower interest rate, but you may not pay less interest over the life of the loan. Early in a loan schedule, your payments go heavily toward interest. Later in the loan, your payments go mostly toward the principal. Resetting that table means you go back to paying more toward interest, which could result in paying more interest over the life of your loan, even with a lower rate.

Shopping for Rates and Terms

If you decide it still makes sense to refinance, you want to shop around to get the best rate. Getting a quote uses a soft credit check, so it won’t hurt your credit score. Platforms like Juno make it easy to shop around different lenders, and their purchasing power can sometimes secure different incentives.

Once you find the lowest rate, pick a loan term that matches your repayment window. For example, if you are a mid-level associate and want to leave Big Law before making partner, you would choose a repayment term that aligns with your timeline. Private lenders offer a variety of options, typically including 3, 5, 7, 10, and 15-year terms.

Remember that refinancing locks you into that specific payment without federal safety nets. You have to be certain you can make that payment regardless of what happens in your career.

Option 2: Make Aggressive Principal Payments

An alternative method to paying off your student loans faster is to keep your current loans but make extra payments toward the principal. To build this strategy, you need a loan calculator that lets you run different scenarios.

You want a calculator that not only lets you apply additional principal payments each month, but also schedules one-time yearly payments. Big Law bonuses operate on a lockstep model and get exponentially bigger each year, so using a portion of your bonus each year is a highly effective strategy. I like this calculator because it lets you do all of that.

If you have multiple federal loans, you can either calculate each loan individually (which yields the most accurate plan but requires multiple calculations) or combine them using an average interest rate and loan term for a solid baseline estimate.

If you want to watch a step-by-step process on how to use the calculator, check out this video.

Running the Numbers

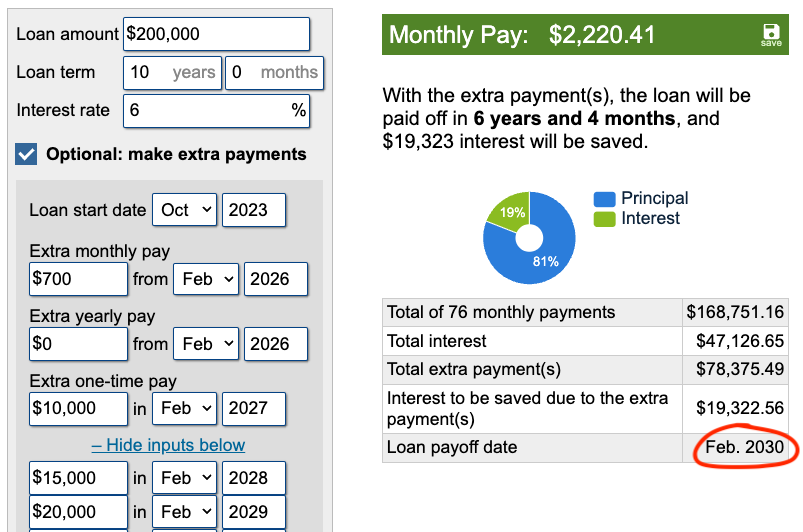

Let's look at a scenario for a fourth-year associate who started repaying their loans in October 2023. Assume your original loan balance was $200,000 and the interest rate was 6%.

In this case, your monthly payment is $2,220 on a standard 10-year federal repayment plan, with a payoff date of October 2033. However, your goal is to leave Big Law by 2030 before you make partner.

After playing with the numbers, you arrive at this strategy:

- Making $700 extra principal payments each month. Your new monthly payment is $2,920 ($2,220 + $700).

- Making a one-time $10,000 payment from your bonus in February 2027.

- Making a one-time $15,000 payment from your bonus in February 2028.

- Making a one-time $20,000 payment from your bonus in February 2029.

As a result, the pay-off date goes from October 2033 to February 2030, which aligns with your desire to leave Big Law by 2030.

This aggressive loan repayment strategy would save you roughly $19,000 in total interest, with a total interest payment of roughly $47,000.

In other words, your “net cost” to go to law school would have been just $47,000.

Not bad considering the career and income potential your law degree has created.

Comparing Your Options

Once you calculate both scenarios, compare them side by side.

Let's say your refinancing option is a 5-year loan, and you will pay a total of $17,000 in interest over the life of the loan. If staying on your current loans and paying them more aggressively generates $19,000 in interest from now until the projected payoff date, there is only about a $2,000 difference between the two options.

Your decision then comes down to a simple question: Is saving $2,000 in interest worth losing the flexibility and protections of your federal loans?

Note that to compare the two options, you only need to calculate interest moving forward. Any interest paid in the past is irrelevant. To find out, you will need the full amortization table of your current loans, which you can find in the calculator.

Take Control of Your Timeline

Paying off your student loans faster is a great goal. But doing it the wrong way could quietly cost you tens of thousands of dollars in extra interest or lock you into a rigid payment schedule that limits your career options.

Need Help Weighing the Options?

If you are not entirely sure which option makes the most sense for your transition timeline, schedule a free introductory call with us. We're here to answer questions and talk through which path may work best for you—based on your actual numbers, goals, and career plans.

👉 Schedule your free introductory call

👉 Learn more about our services & pricing

SharpEdge Financial LLC is a registered investment adviser registered with the State of Texas. Registration does not imply a certain level of skill or training. The views and opinions expressed are as of the date of publication and are subject to change. The content of this publication is for informational or educational purposes only. This content is not intended as individualized investment advice, or as tax, accounting, or legal advice. Although we gather information from sources that we deem to be reliable, we cannot guarantee the accuracy, timeliness, or completeness of any information prepared by any unaffiliated third-party. When specific investments or types of investments are mentioned, such mention is not intended to be a recommendation or endorsement to buy or sell the specific investment. The author of this publication may hold positions in investments or types of investments mentioned. This information should not be relied upon as the sole factor in an investment-making decision. Readers are encouraged to consult with professional financial, accounting, tax, or legal advisers to address their specific needs and circumstances.